Automating banking services while personalizing the customer relationship: the new paradigm of banks

01 / 05 / 2021

While digitization was initially reserved for back office services such as transaction management or operation administration, banks are currently going through out a real digital transformation of the customer relationship. This transformation aims to make the customer the topmost concern so banks can enrich their customer relationship by reinventing all journeys

1. New customer expectations: speed and recognition

A successful customer relationship has become one of the most important success factors for banks. According to a Harris survey, 39% of customers change banks after a bad customer experience. Therefore, banks must adapt to the requirements of customers to best meet their needs and retain them.

Nowadays, customers want to interact with their banks in real time through smooth, transparent contact similar to the experiences they have with companies from other lines of business. Therefore, they demand to get appointments with their advisors in less than 48 hours or to receive the confirmation of a request via SMS. They also want more autonomy and the ability to perform simple operations directly on their mobile phones. Indeed, according to an IFOP survey, 96% of French people browse their banks’ websites or use their banks’ applications.

Finally, in addition to fast response times, customers express a desire for personalization according to their life projects and for tailor-made advice on their financial situations. This explains why customers go to branches less frequently but want to experience contacts with higher value added with their bank advisors.

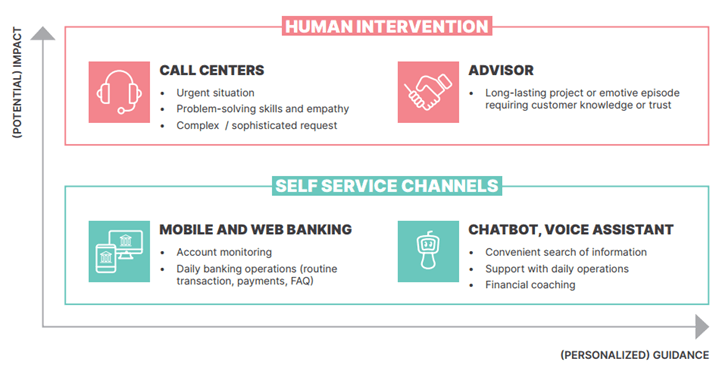

HOW CAN BANKS COMBINE CUSTOMIZATION

AND AUTOMATION IN THEIR CUSTOMER STRATEGY?

2. What strategy to adopt to satisfy banking customers?

These new expectations and the price appeal of online banks have contributed to the development of these new players. In October 2020, the number of customers of Boursorama Banque, the leading online bank in France, surpassed the 2.5 million mark.

During the lockdown period, some customers turned away from their in-branch advisors and increasingly used remote communication channels, thus forcing banks to become more digital.

Automation with complete security

In the face of these new habits and the threat of digital players, traditional banks first had to automate part of the customer service. Thanks to Cloud and omnichannel customer relationship management platforms, processes have been centralized and made easier. They provide a 360-degree view of the customer as well as optimized data use. The implementation of “self-service” with strong authentication has also enabled banks to become more accessible by allowing customers to perform secure operations 24 hours a day, 7 days a week.

To improve its customers’ autonomy, BNPP has launched with Worldline a virtual assistant called Telmi. Thanks to natural language processing, this assistant can, at any time, answer questions on the bank’s website, application or social media. This chatbot can answer about 500 simple questions and automatically redirect the user to a human advisor when necessary. To customize the conversational experience, BNPP asked Voxygen to create a tailor-made voice for the Telmi. This voice is also available on connected speakers such as Google Home. The user can launch this assistant by saying “Talk to BNP Paribas” and then ask a question or make an appointment directly.

However, this robotization should not be total because customers always want to maintain authentic human contact with their advisors. As mentioned in a Markess survey, 46% of customers find it uncomfortable to interact with a machine. The challenge is thus to find the most relevant use cases to automate and leave to advisors the opportunity to really advise customers.

Personalizing contact points

Confidence and the attention paid to needs remain major expectations. Banks differentiate their offers by offering, for example, the customization of the bank card’s appearance and payment characteristics. A Salesforce survey reveals that 79% of customers are willing to share their data in exchange for a tailor-made customer journey.

This is why BNPP is currently testing, in particular for asset management, an expert banking advisor in exchange for a 12-euro monthly subscription. This service, which is normally intended for high-net-worth customers, is likely to become widespread so branch advisors, who are often used too much for administrative tasks, regain value.

Adopting a “Phygital” strategy

The “Phygital*” strategy then seems to achieve the right balance. Banks opt for a remote omnichannel communication strategy using digital tools while maintaining the physical relationship in branches. The latter remain the preferred place for high-value-added exchanges, for which the dialogue with the customer is made easier and where the advisor’s role takes on its full meaning. Low-value recurring tasks are automated to free up their time.

3. What tools to implement to combine automation and personalization?

The WL Contact solution provides many features to automate and personalize the most frequent requests. It also makes certain actions easier for agents so they can work more efficiently.

Knowing your customer

The major condition for a successful customer relationship is knowing your customer. It is indeed fundamental to have a global, unified view of your customer by knowing, for example, their preferences or situation. Thanks to the easy integration of Worldline Contact into the company’s information system, the exchange can be contextualized through in-depth customer knowledge. The agent can view all the previous interactions with the customer as well as the evolution of their requests. The advisor can quickly meet the customer’s requests while adapting the content of the message to the profile and context.

Since pertinent integration into the information system makes it possible to recognize the customer, it is then possible to define how the bank wants to personalize its experience: criteria define whether “self-care” service should be preferred, the interaction should be routed to the customer’s preferred advisor, or the customer should be referred to an expert. What reception or waiting experience does the bank wish to set up? Should a specific piece of information or offer be proposed to this customer? Should the bank offer to call them back later? All these scenarios can be proposed depending on the bank’s challenges.

Personalizing the relationship across all channels

The omnichannel nature of the solution makes it possible to communicate through the customer’s preferred channel. The customer relationship must continue on all digital interfaces with the same level of personalization.

While the previous examples illustrated how the IVR (Interactive Voice Server) system can be customized, this individualization should be carried out on all the points of contact between the bank and its customers.

On the web channel, the chat makes it possible to proactively engage the customer as they navigate on their bank’s site. Depending on various navigation criteria, the bank will propose a simulation or a conversation with an advisor.

On the e-mail channel, the message, although it is automated e.g. through canned reply suggestions, can be personalized using information relating to the customer (their name, customer number, request identifier, etc.). It is also possible to tell them how much time will be needed to process their inquiry.

Finally, even though reply automation allows banking services to be accessible 24 hours a day, 7 days a week, it is important to give the customer an elaborate, complete reply. When the customer is not satisfied or wants more information, they can use other channels and talk to an advisor. For example, when a customer contacts one of our large banking customers via e-mail, a canned reply is suggested first to reduce the waiting time normally induced by an exchange of e-mails with their advisor. If the reply is adequate, the customer will not have to wait until their advisor is available to process their request. On the other hand, if this automatic resolution does not suit them or is partial, they can continue the exchanges via e-mail.

The advisor remains the best point of contact for complex matters because automation does not solve all requests.

4. What are the benefits for the banks?

Although the digitization of the sector has forced banking players to adapt quickly, the transformation of the relationship is also becoming a growth engine.

Since transaction processing times are reduced and processes simplified, banks are more efficient. Improving the access to information provides them with better tracking and greater availability. In addition, thanks to digitized, flexible processes, banks are more responsive to changes.

For this transformation to succeed, banks need to be supported by a partner who is a customer relationship expert and will help them take advantage of all these changes.

Today, banks are largely digitized, which is an advantage in terms of agility, customer autonomy, and reduction of operating costs. However, advice and proximity between the customer and their advisor must remain predominant. The challenge is then to find the best combination between automation and personalization to satisfy customers.

Learn more about our Mobile Banking solution.

Watch our webinar on the five steps to orchestrating self-care on digital banking channels. This is an opportunity to learn more about the methodology that should be implemented to improve the accessibility of your services while increasing customer satisfaction.

* Phygital: marketing concept that links the physical environment to digital tools