Why insurance companies should look to Open Banking

01 / 09 / 2021

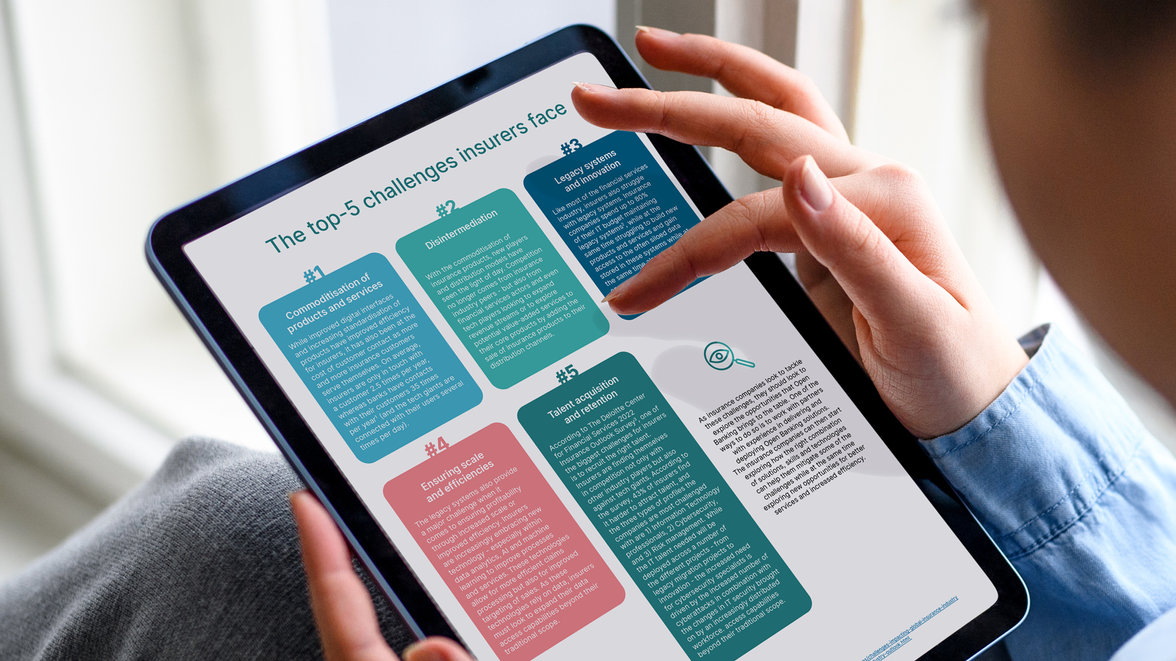

The insurance industry faces many of the same challenges as banks and can benefit from the learnings and technological advancements made through Open Banking for insurance companies.

Introduction

When the EU Commission introduced the Revised Payment Service Directive - PSD2 - it kickstarted the acceleration of open banking in Europe and indeed the world. Open Banking is not a result of PSD2 but a culmination of much more significant and more long-lasting trends across the digital economy. These trends are fuelled by innovations made by small and large tech companies in close combination with changes in consumer behaviour and expectations. Furthermore, these trends have also been further accelerated by the innovation and proliferation of financial services through the fintech boom of recent years. But development and digitisation will not end there - as we move towards Open Data, it is clear that the insurance industry is indeed facing many of the same challenges as banks, but at the same time stand to benefit from the learnings and technological advancements made through Open Banking.

The top-5 challenges insurers face

- https://www.der-bank-blog.de/zukunft-bancassurance-2/digital-banking/37682837/

- https://www.moodysanalytics.com/risk-perspectives-magazine/integrated-risk-management/principles-and-practices/challenges-impacting-global-insurance-industry

- https://www2.deloitte.com/us/en/insights/industry/financial-services/financial-services-industry-outlooks/insurance-industry-outlook.html

The opportunities

Open Banking provides the most mature set of APIs across Europe. Insurers can - with the right partners - tap into these and start building their own capabilities for API integration and foster innovation while at the same time leveraging the IT talent of their partners. The Open Banking APIs can provide insurers with new opportunities to reduce operational costs by tapping into the account-based payment rails or improving processes through access to verified customer data, e.g. checking the validity of an IBAN before making a payout.

The customer data can - with the consent of the consumer, of course - also be explored in terms of building up data-analytics capabilities without having to wait for the in-house legacy migration projects to fix the lack of data access. These data analytics opportunities cover a number of potential use cases - including

Would you like to learn more?

Simply fill in a few details and our experts will get in touch.