Today’s consumers and merchants expect payment experiences to be increasingly frictionless or invisible to the point where customers do not need to trigger or complete a payment themselves. Autonomous payments are payment transactions triggered by an authorised virtual payment agent acting on behalf of the consumer.

"Autonomous payments are payment transactions triggered by an authorised virtual payment agent acting on behalf of the consumer."

This payment agent can be part of an IoT device or a piece of software. Or it could take the form of a smart contract which automatically triggers payments when certain conditions are met (so-called “programmable money”).

In either case, the rules and boundaries for the payment are initially set by the user/owner giving the payment agent the authority to trigger and complete the payment on their behalf. Autonomous payments help decrease friction and improve the consumer experience because you can complete the transaction efficiently and quickly with little to no effort by the user.

Industries across various sectors are demanding innovative payment solutions to support the ever-changing needs of their consumers, the evolution of their market and societal developments. We believe that in many situations autonomous payments will become the norm, delivering:

- For consumers, a genuinely frictionless experience for repetitive or low-value purchases. Saving them time and effort (for example, walk-in/walk-out solutions for public transport)

- For merchants, a seamless customer experience leading to higher conversion rates, increased revenues and more repeat custom

- For all businesses creating new offerings based on IoT, Artificial intelligence and APIs, the ability to embed automated payments into their value propositions to create truly innovative, automated, end-to-end experiences for their clients

Autonomous payments enable innovative business models in both the sharing and circular economies through pay-per-use models. We believe that autonomous payments will impact merchants’ businesses in the following ways:

- Further improving the customer experience by reducing friction, improving the speed of transactions and appealing to those who self-serve, such as fully autonomous shopping experiences and vending machines.

- Enabling instant transaction processing in more scenarios, reducing the need for infrastructure and resources (such as with automated road toll charges).

- Growing business by opening up the integration of new ecosystems and business sharing platforms.

- Increasing consumer engagement with autonomous reward schemes through the use of artificial intelligence.

- Supporting new business models. For example, Mobility-as-a-Service or Printing-as-a-Service.

- Controlling costs for merchants by improving monitoring and providing better insights for treasury and financial management and reducing the administrative processes connected to payments and auditing.

User adoption for autonomous payment remains the critical challenge

By 2023, the IoT payments market is expected to reach $27.6 billion. The market segments that will benefit from this development include retail, automotive, transport, smart city and smart housing(https://www.intellias.com/iot-payments-what-s-ahead-for-contextual-commerce/). Despite high expectations for this emerging opportunity, how popular autonomous payments will become is still unclear.

"By 2023, the IoT payments market is expected to reach $27 billion."

On the one hand, most connected devices are not relevant for autonomous payments use cases (e.g. temperature sensors, smart door locks, home security cameras, etc.). On the other hand, relevant IoT devices like connected cars, intelligent fridges or health care devices are still finding their way into the autonomous payments landscape.

From the technological point of view, IoT, AI, Blockchain, 5G, LPWAN networks and technical standards are already mature enough to be deployed on a large scale. Whereas other technologies for platform interoperability, voice authentication and face recognition still require further development. Other challenges are not technological and relate more to consumer willingness to adopt.

We see the main challenges for autonomous payments as:

Consumer adoption – A user-friendly and intuitive solution would certainly help accelerate consumer adoption, but it is essential to understand what prevents a consumer from using autonomous payments.

Openness and interoperability between platforms – The economy of platforms is dominating the online commerce space. We believe that autonomous payments will follow the same philosophy. The industry needs to leverage existing API standards to facilitate payment transactions triggered by connected objects across platforms and stakeholders.

Impact on e-commerce platforms – E-commerce platforms such as Amazon, Walmart, Alibaba, and Cdiscount deploy large-scale automated processes to stay competitive. For example, the shopping cart of Walmart’s online shop uses dynamic factors such as customer location, supplier location, delivery prediction and stock availability to come up with the cheapest suggestion. To increase purchase conversion, we believe that merchants will provide consumers with AI-based virtual shopping assistants which can autonomously handle purchases based on various factors, such as the best price/delivery time ratio.

Lack of an endorsed ecosystem for autonomous payments – Building an autonomous payment ecosystem requires a new mindset. Today, there is a rebalancing of power going on between banks, scheme owners and FinTechs. In the case of autonomous payments, the specific challenge concerns building business models and adequate technology enablers around micropayments.

Keeping up with new regulations –The 2014 regulation on electronic Identity and Security (eIDAS https://eur-lex.europa.eu/legal-content/NL/ALL/?uri=celex%3A32014R0910) ensures that cross-border transactions can be performed safely and securely. The EU is now proposing a framework for a European Digital Identity to offer 80% of all EU citizens electronic identity (eID) for all online public services.

Merchants and payment providers can use eID solutions to develop and offer new services that would authenticate the consumer securely and conveniently whilst removing friction and delays. This would help gain customers’ implicit trust and make them comfortable with the idea of autonomous payments.

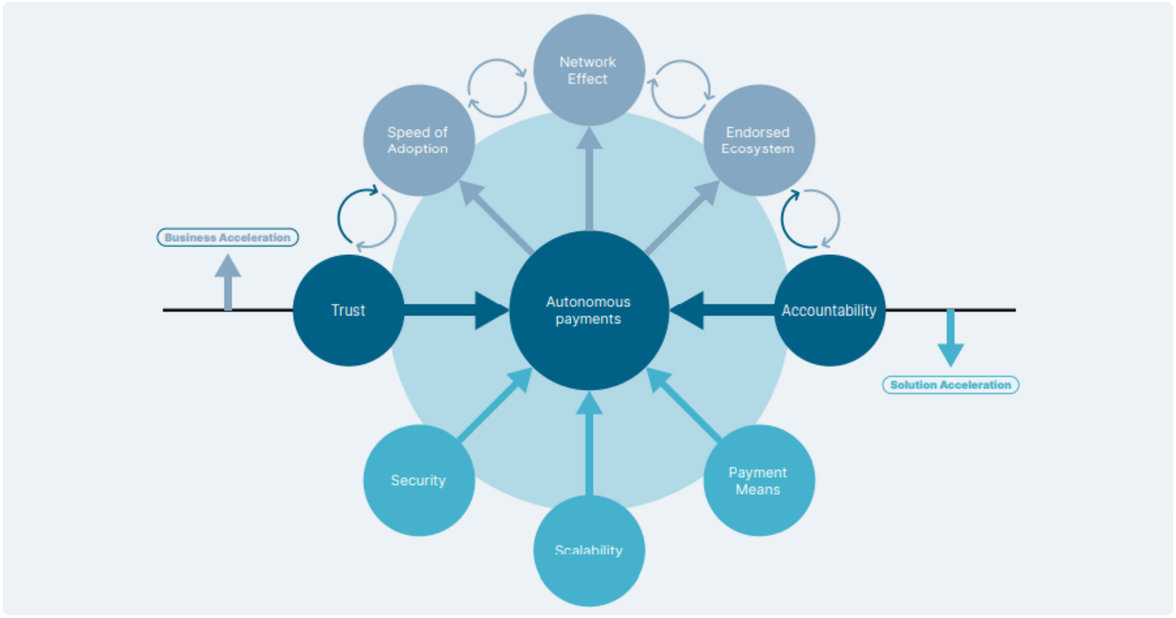

We expect that the adoption of autonomous payments will be driven by factors relating to trust and accountability. Together with the underlying issues of security, scalability and integrated payment means. Similar to other business ecosystems, autonomous payments need to be endorsed and pushed by key stakeholders. Ultimately, the speed of adoption, powered by the endorsed ecosystem, will generate the network effects of billions of connected devices and millions of users and merchants.

Adoption drivers for autonomous payment

More chapters about Seamless Interactions Amidst Accelerated Digitalisation

More resources

-

Manufacturing

Collect data across your entire product value chain.Learn more Opens in a new tab -

The IOT payment revolution

The IoT Payment Gateway Revolution is the future of autonomous payments. The IoT payments market is expected to be worth $27.6 billion by 2023. Learn more here.Learn more Opens in a new tab